Leaving a job can be bittersweet—or sometimes, just plain bitter. But if you have a defined pension benefit, leaving a job can also be complicated. What happens to your pension plan when you move on from a company before you’re ready to retire? You may wonder if you’ll get the money right away, and if so, what you should do with it. You may also have questions about the tax consequences of taking your money in a lump sum (if that’s an option).

There was a time when some people wouldn’t consider leaving a job with a defined benefit pension, but people change jobs much more frequently than in the past, and the types of benefits employers provide have changed. If a better offer comes along before retirement, it’s up to you to decide what to do with the pension you have accumulated.

What’s a Defined Benefit Pension?

A defined benefit pension is what most people think of as the traditional, old-school pension that your parents or grandparents had. You know, the type that guarantees workers who stay with a company a lifetime income stream during retirement.

Note

Defined benefit pensions are not as common these days. They have been replaced by defined contribution plans, such as 401(k)s, which put much of the savings responsibility on the employee and do not come with any guarantees of a set amount of retirement income.

Are You Vested?

According to the Department of Labor, in a defined benefit plan, an employer may require that employees have five years of service to become 100% vested in the employer-funded benefits. Employers may also choose to offer a graduate vesting schedule. With this schedule, employees would be 20% vested after three years, 40% vested after four years, 60% vested after five years, 80% vested after six years, and fully vested after seven years of service. Employers are free to offer plans that are more generous than this one, as long as they adhere to these minimums.

Note

You are only entitled to the vested portion of your pension at the time you leave your employer.

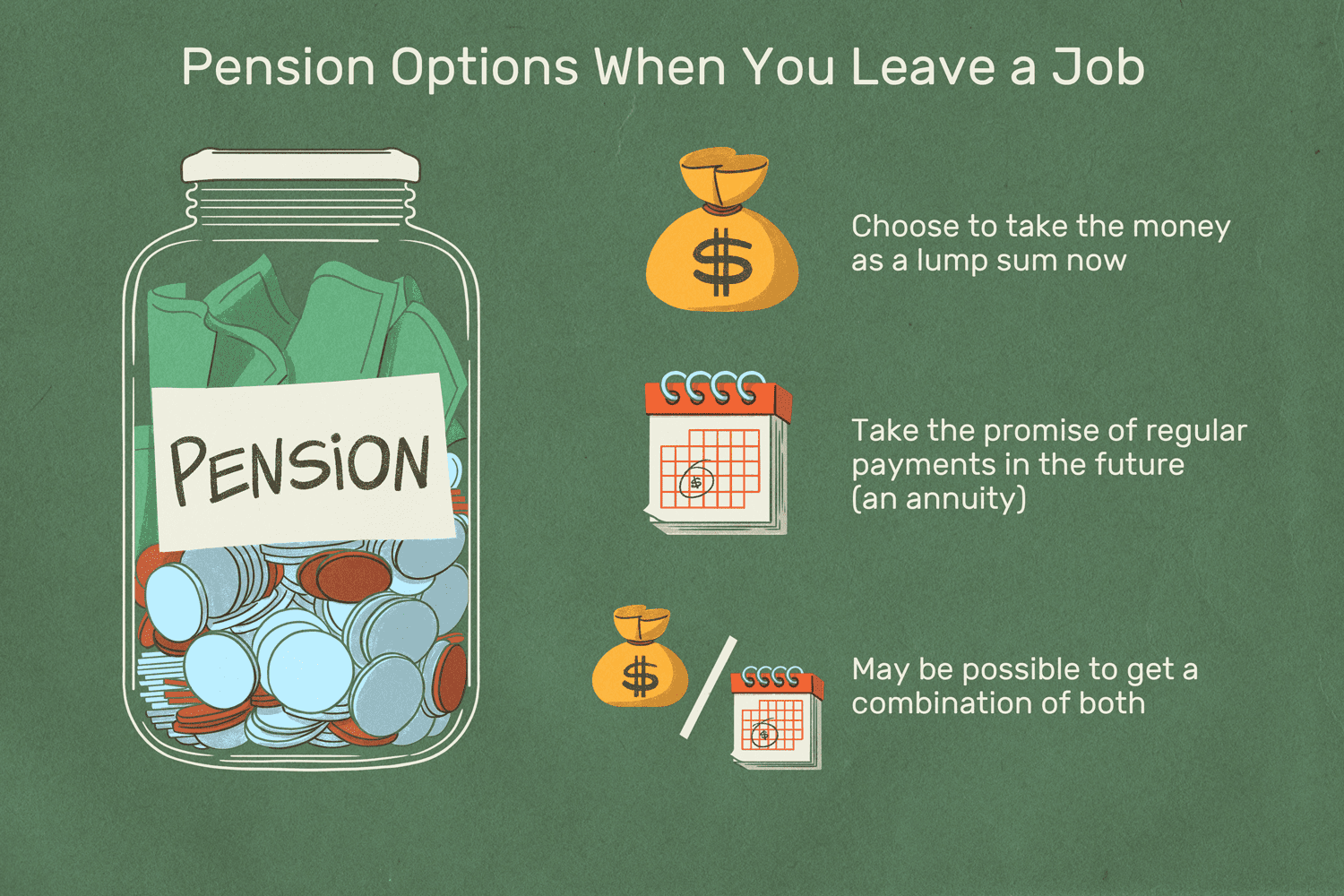

Pension Options When You Leave a Job

Typically, when you leave a job with a defined benefit pension, you have a few options. You can choose to take the money as a lump sum now or take the promise of regular payments in the future, also known as an annuity. You may even be able to get a combination of both.

What you do with the money in your pension may depend on your age and years until retirement. If you are young and have a relatively small amount of money at stake, a lump sum may be the easiest choice.

Note

Keep in mind that most annuity payments are fixed and do not keep up with inflation. Today’s small annuity will look even smaller in the future.

Investing Your Pension Funds

In 30 to 40 years, the purchasing power of your pension could be greatly reduced. Invest it yourself, perhaps with the help of an accredited financial advisor, and you may be able to get a better long-term return on your money. However, if you are a disciplined investor, managing your pension resources will make more sense than if you are prone to fear-based reactions to market moves.

Take the Annuity

On the other hand, if you are closer to retirement and looking for guaranteed income, the annuity may be a more attractive option. You don’t have to worry about investing the money yourself in the precarious pre-retirement years.

You may also have a better sense of the company’s near-term health and ability to meet its pension promises. Pensions are insured by the government through the Pension Benefit Guaranty Corporation, but when companies go under, employees and former employees usually don’t get everything they had been promised. Sometimes, companies will offer extra benefits to encourage older employees to stay in their plan. If your research indicates your plan is underfunded or is likely to be in the future, then you might be more likely to select a lump sum.

What to Do With a Lump Sum Pension Payment

If you do take the lump sum, consider transferring the money directly from your pension into a rollover Individual Retirement Account (IRA) to keep it from being taxed. If your company writes you a check, you have 60 days to move the money into a tax-favored account before the money is taxed.

Should You Spend Your Pension Funds After Cashing Out?

Unless you really need the funds, it’s best to avoid spending the lump sum before retirement. Not only are you missing out on long-term investment growth, but you will also have to pay taxes on the cash plus a 10% early withdrawal penalty. If you have significant assets in your plan, you could face a high tax bill.

Within a rollover IRA, the funds can be invested in any way you choose. You could even purchase an annuity within the IRA to capture some of that guaranteed income on your own.

Some retirement plan administrators, including Vanguard and Fidelity Investments, offer advice and online tools to help employees decide between an annuity and a lump sum. It’s worth playing around with a few of them before making a decision. You can also contact plan administrators for advice based on your specific circumstances and goals.

Key Takeaways

- A defined benefit pension plan guarantees employees a fixed amount of income during retirement based on factors such as salary history and years of service with an employer.

- Understanding vesting requirements is crucial; you are only entitled to the vested portion of your pension when leaving an employer.

- Consider wisely: Invest your pension funds for potential growth or opt for an annuity for guaranteed income. Consider factors such as age, financial needs, and company stability.